As the second-largest bank in China, China Construction Bank

faced persistent challenges stemming from legacy systems,

including slow business innovation cycles and mounting pressure to

process massive transaction volumes. In response, CCB partnered with

MuRong Technology in 2019 to accelerate the development of a

next-generation digital banking system.

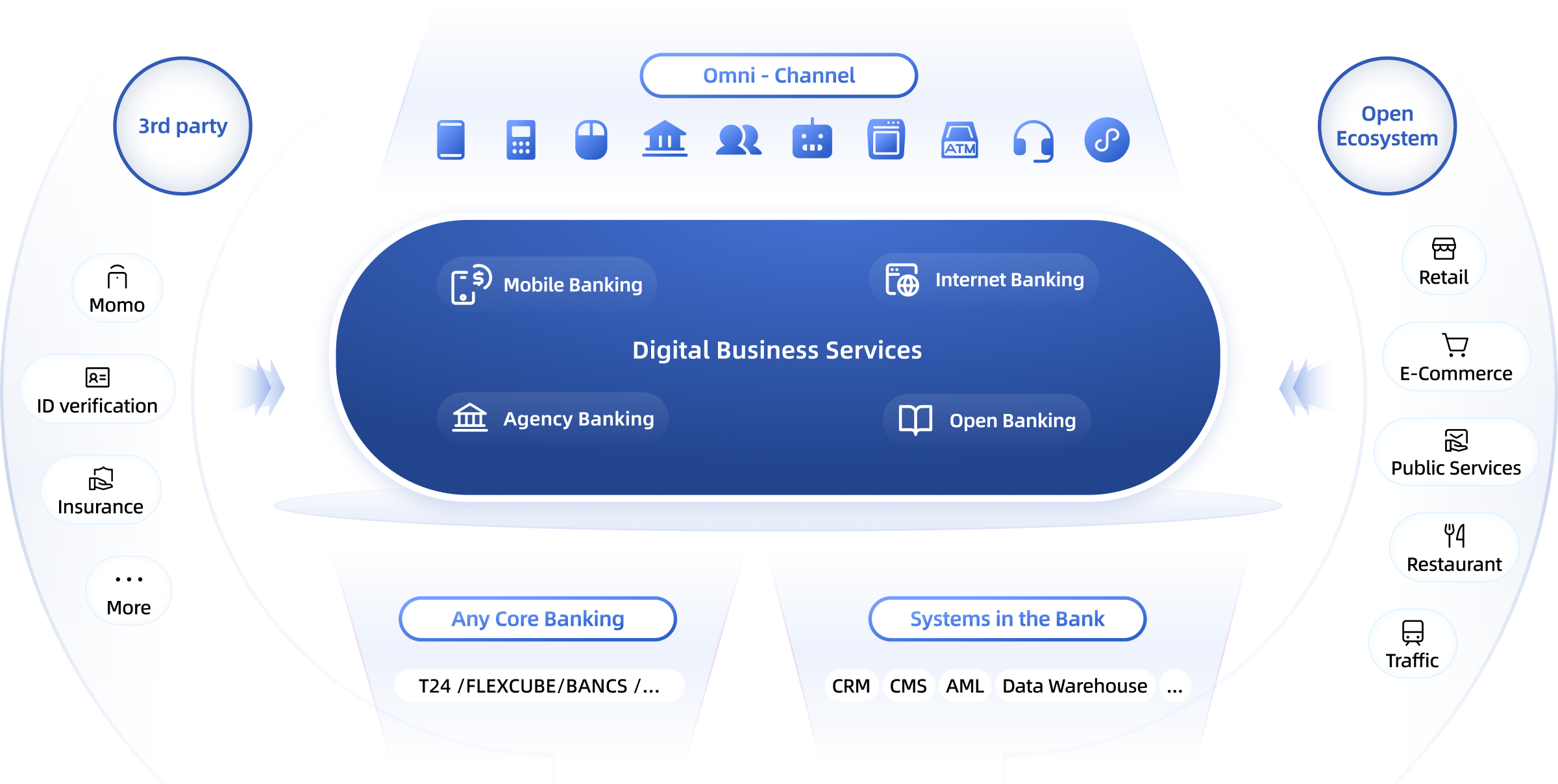

MuRong delivered a secure, flexible, and open digital banking

platform that enabled the comprehensive rollout of online financial

services and effectively supported digital finance requirements across

multiple industry scenarios. This transformation laid a solid foundation

for large-scale innovation, high-concurrency processing,

and ecosystem expansion.

Transformation Achievements

By 2024, the platform had supported the launch of

more than 200 digital financial products, serving over 100 large

enterprise clients and more than 80,000 merchants.

Its application spans dozens of sectors, including e-commerce,

new retail, automotive services, and government platforms.

The system successfully handled extreme peak transaction

loads during major promotional events such as “618” and “Double 11”

with zero service disruptions, while cumulative transaction volumes

surpassed RMB 1 trillion. As a result, CCB significantly enhanced

customer experience, reduced operational costs, and reinforced its

leading position in the digital finance landscape.

As the third-largest bank in Kenya, NCBA faced structural constraints caused

by slow legacy system responsiveness and limited product flexibility,

which hindered the expansion of its digital business initiatives.

To overcome these limitations,

NCBA partnered with MuRong and adopted the Greenfield

Model to drive a comprehensive digital transformation.

MuRong delivered a modern digital banking platform and Super App for NCBA,

enabling end-to-end digital financial services, including customer onboarding,

mobile deposits, online lending, digital payments,

and intelligent marketing. This transformation significantly

enhanced NCBA’s digital agility and positioned the bank as a

leading benchmark for digital banking innovation across Africa.

Transformation Achievements

By 2024, NCBA’s digital business had achieved sustained annual growth of 20 to 30 percent,

serving more than 68 million digital financial customers in Kenya.

At the same time, its digital banking footprint expanded rapidly beyond

domestic markets into six additional African countries, including Tanzania,

Rwanda, Uganda, Côte d’Ivoire, and Ghana. Through this expansion,

NCBA has played a pivotal role in advancing inclusive finance across the region,

delivering accessible and scalable digital financial services to a broader population.

KCB is the largest commercial bank by assets in East Africa.

Constrained by legacy core banking systems,

the bank faced challenges including slow business innovation,

inconsistent customer experience,

and limitations on cross-regional expansion.

To address these issues, KCB partnered with MuRong and adopted the Fusion

Model to advance its digital transformation agenda.

Built on MuRong IDO, the project rapidly delivered a modern digital banking

platform while maintaining seamless collaboration

with existing core systems through high-performance data interfaces.

This approach achieved an effective balance between transformation speed and business continuity,

enabling large-scale digital innovation without operational disruption.

Transformation Achievements

KCB’s digital banking services have been successfully rolled out across six markets,

including Kenya, Tanzania, Burundi, South Sudan, Rwanda, and Uganda,

serving more than 10 million users across the region.

The bank has established a diversified digital ecosystem encompassing online account opening,

digital lending, money transfers, multi-scenario payments,

value-added financial services, marketing enablement,

and intelligent customer service. The platform supports multilingual

operation and multi-theme personalized customization,

significantly enhancing customer engagement across diverse markets.

Underpinned by a cloud-native and microservices architecture,

the system enables elastic resource scaling, real-time transaction processing,

and end-to-end operational monitoring.

This transformation has set a benchmark for the smooth

and scalable digital modernization of large commercial banks.